Smart Ways for Students to Graduate Without Crushing Debt

Amber Ramsey, Guest Writer

Regis University students, and the staff who support them are feeling the student debt crisis up close, even while juggling classes, jobs, and campus activism. College affordability keeps tightening, and the financial challenges in higher education can make a degree feel like a long-term bill that starts before graduation. When costs rise faster than budgets, borrowing can seem like the only option, and that pressure can shape choices about majors, housing, and opportunities. Debt-free college options help protect future flexibility and keep the focus on learning.

Quick Summary: Graduate Strong Without Debt

● Apply early for scholarships and grants to cut costs without taking on loans.

● Use work-study programs to earn money while keeping academics as the priority.

● Pick flexible side gigs for students to cover everyday expenses and reduce borrowing.

● Choose in-state tuition benefits and other affordable college strategies to lower the total price.

Build Your No-Loan Budget: 10 Tactics That Actually Work

A “no-loan” budget isn’t about perfection, it’s a plan that funnels your time toward the fastest- payoff options you saw earlier (grants, scholarships, work-study, and flexible income). Use these tactics to shrink the bill before you ever consider borrowing.

1. Price out online classes strategically: Start by comparing the per-credit cost for online

vs. in-person classes and the hidden costs you may avoid (commuting, parking, meals out). If an online section is cheaper or saves you several weekly expenses, plug that difference directly into your budget as “tuition covered.” Aim to choose online courses for gen-eds or lecture-heavy classes where you won’t lose needed hands-on time.

2. Treat scholarships like a weekly job (with a quota): Set a simple goal: 2 applications per week for 6 weeks. Keep a “reusable kit” folder with your unofficial transcript, a master resume, and 3 short essay drafts you can adapt (leadership, challenge, community impact). The secret is consistency, small awards stack, and they reduce how many hours you need to work later.

3. Use work-study to protect your grades (and your schedule): If you qualify, prioritize campus work-study jobs with downtime you can use for homework. Ask in the interview what a normal shift looks like and whether there are quiet hours. A steady 8–12 hours a week can cover basics without pushing you into burnout.

4. Build a student side business you can run between classes: Pick one service you can deliver in 60–90 minute blocks: tutoring, note-cleanup/editing, poster/flyer design for campus clubs, or game-day photography for friends. Keep it simple: one price list, one way to get paid, and one weekly availability window. The fact that 36% of adults have a side hustle is a reminder you’re not “behind”, you’re building a normal, modern income stream.

5. Reduce housing costs with one bold change: Housing is usually the biggest line item, so pick one lever to pull this month: add a roommate, move a few blocks farther from campus, or choose a smaller floor plan. If moving isn’t possible, negotiate within your current place, offer to sign earlier, extend your lease, or take on a small property task in exchange for a lower rate. Even $100/month is $1,200 a year you don’t have to borrow.

6. Cut course material costs with used textbook rentals + backups: Before buying anything new, check rentals, used copies, older editions, and the library’s reserve options. Many students feel this squeeze, 54% of respondents in a national survey reported significant concerns about textbook prices. If a book is only used for a few chapters, ask your professor on day one whether an older edition works or if readings are available through course links.

7. Add two “stackable savings” habits: fees + food: First, do a quick fee audit: waive anything optional and set reminders to avoid late charges. Second, set a realistic food plan, pack two days of lunches each week and make one low-cost “default dinner” you can repeat when life gets hectic. These are small wins that free up cash for tuition payments and keep your budget from collapsing under stress.

When you combine lower tuition paths, predictable income, and a few expense cuts, you’ll be in a stronger position to choose between major cost-saving routes, like online programs, in-state options, or employer tuition help, without guessing.

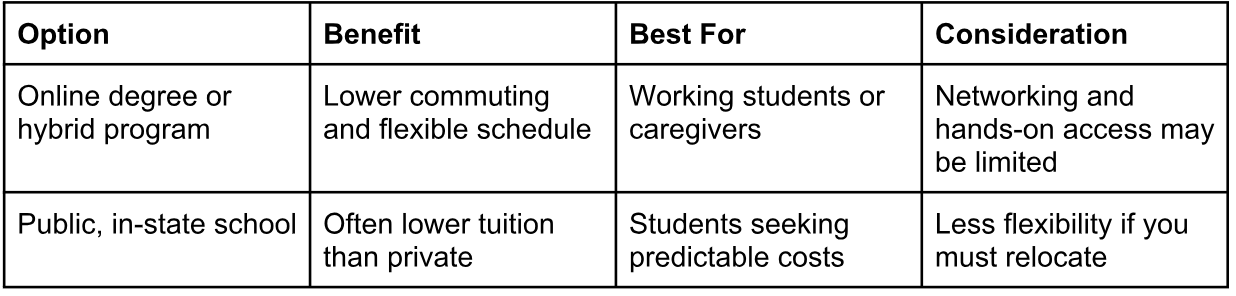

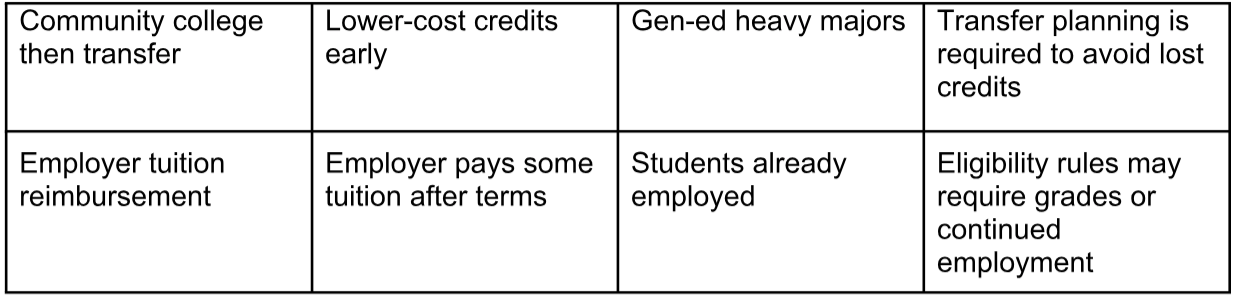

Cost-Saving Education Options Compared

These options all lower what you pay, but they do it in different ways: reducing tuition, reducing living costs, or shifting costs to an employer. For students and campus staff focused on access, creativity, and social justice, the best choice is the one that protects time, mental bandwidth, and degree momentum, not just the sticker price.

A practical way to decide is to rank your top constraint: time, total cost, or stability. If you are employed, tuition help is worth checking because nine in ten organizations offer an educational benefit. Choosing the option that fits your real life keeps the plan sustainable, and that is a financial win.

Common Money Questions Students Ask

Q: What are some practical ways to minimize living expenses while attending college?

A: Start with the biggest line items: housing, food, and transportation. Share a place with roommates, use campus pantry and meal-prep routines, and cut subscriptions you do not use. Choose low-cost commuting options and ask about free transit passes, emergency grants, or textbook lending through the library.

Q: How can I find and apply for scholarships and grants to ease financial pressure?

A: Treat it like a weekly routine: search your school portal, department pages, and community foundations, then apply in batches. Remember that financial aid can cover more than tuition, so include need-based grants alongside scholarships. Keep a folder of required PDFs, label versions by date, and use an online PDF tool to manage PDF files online by merging, signing, and storing forms securely.

Q: What strategies can help balance work responsibilities with academic commitments to reduce stress?

A: Pick predictable shifts, cap hours to protect study time, and build your schedule around your hardest class first. Communicate early with supervisors and professors, and use office hours to stay ahead. If possible, choose campus jobs that allow homework during quiet periods.

Q: What steps can I take to avoid feeling overwhelmed by college-related expenses?

A: Make a one-page “money map” listing fixed costs, due dates, and a small weekly buffer for surprises. Use a checklist to track submissions since financial aid checklists can show what has been received and what is still missing. When stress spikes, ask the financial aid office about payment plans and short-term hardship options before turning to loans.

Q: How can I effectively manage tuition payments if my employer offers a reimbursement program?

A: Read the policy closely for grade requirements, eligible courses, and reimbursement timing so you can plan cash flow. Ask whether the school can delay portions of your bill, and set aside a “reimbursement holding” amount each paycheck. Keep every receipt, syllabus, and grade report as labeled PDFs so you can submit quickly and avoid delays.

Build Debt-Free Momentum With One Smart Money Move

College costs can feel like a constant squeeze, and it’s easy to drift into loans just to keep up. The good news is that personal finance for students works best as a simple system: organize your paperwork, keep applying funding strategies, and stick to a realistic plan for successful college budgeting. Do that consistently, and debt-free college motivation turns into real progress toward college achievement without loans. Small choices, repeated weekly, are the fastest path to a debt-free degree. Choose one next step this week: apply for one scholarship or grant, set a basic weekly budget, and confirm your next tuition plan. That steadiness builds confidence and resilience that will support school, work, and life after graduation.